Is it "greedflation?"

There is a new term being battered about these days in terms of what is going on in the macroeconomy: greedflation.

It goes to the question: what is the main driving force behind the recent runup in consumer prices? Or more simply: why is there inflation?

The "traditional" or "conventional" answer to these questions is usually some combination of the following:

- The Russian invasion of Ukraine pushed up costs of things like fertilizers, oil, etc. and these costs are being passed on to consumers.

- Supply chain disruptions have caused shortages of goods and competition for these scarce goods has pushed prices upward.

- (This one is the Fed's favorite) The low unemployment rate and high job vacancy rate means labor costs for firms are/will be increasing and thus prices of goods and services are increasing.

- These increases in costs are then the "spark" that is added to the "fuel" that is an increased money supply, resulting in the "fire that burns" which is inflation.

In this "traditional" or "conventional" story, corporate profits may initially increase if sellers base their current selling price on replacement costs not historical costs. So firms produced stuff when costs were "low" but now sell their output at a higher price representing what it would cost them to produce it now. But, the increased mark-ups and resulting increased profits should quickly fade away as higher costs "catch-up" to selling prices.

And this is where it gets weird.

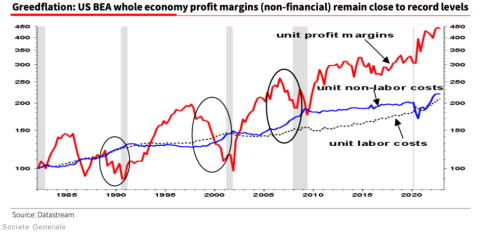

Alan Edwards at Société Générale has pointed out that mark-ups have increased but have NOT fallen. As the graph above from Edwards' recent report demonstrates, not only is the Fed's favorite story of "higher labor costs" not consistent with data, but the really striking thing is what has happened to mark-ups. They are not falling.

It turns out that this is not true for ALL industries across the US, but where it is true, it is eye opening. That has led some, including Edwards, to argue that what is really going on is that a number of firms with market or pricing power have decided to "take advantage" of the news of the war in Europe, supply chain difficulties in other industries, and the Fed's ramblings. These firms, the argument goes, have raised their selling prices even though their costs have not increased significantly. Thus the name: greedflation, or inflation driven by...well...greed. It's not really costs that are driving higher prices, it is greed.

Edwards argues that this just the most recent use (some would abuse) of large firms' market unchecked market power. It has been argued for several years that these large corporations have been putting the screws to their employees (e.g. pushing for increased labor productivity with little or no change in real wages), and to the their suppliers. Now, it is argued, these large entities with market power have turned to putting the screws to their customers by increasing selling prices and consumers have no where else to turn.

A growing number of economists are joining Edwards in warning this type of behavior, if it continues, may very well threaten the underpinnings of capitalism. One only needs to read (or re-read) Adam Smith 1759 masterpiece "The Theory of Moral Sentiments" to understand why these claims are being made.

It will take awhile until we get sound data to determine how wide spread this "greedflation" is and how much of it is contributing to the current inflation rates. But, if it does prove to be significant and has a lasting impact on how our markets function, one might want to ponder: might this turn out to be a major inflection point for modern day capitalism? Perhaps it is time we start to take Smith's 1759 work much more seriously.

Stay Informed

When you subscribe to the blog, we will send you an e-mail when there are new updates on the site so you wouldn't miss them.

About the author

© 2020-2026 Mike Brandl. All Rights Reserved.

Comments